- Register

- Sign In

Interest Rate Announcement: BoC Delivers Second Consecutive “Jumbo” Rate Cut

by RE/MAX Canada

Benchmark Rate Now Sits at 3.25%

In a widely expected move, the Bank of Canada has continued the downward trajectory with a second consecutive half-point cut to its benchmark interest rate, which now sits at 3.25%. This marks the fifth interest rate cut in a row, despite s slight uptick in inflation, which rose to two per cent in October, up from 1.6 per cent in September. Inflation still sits at the Bank’s two-per-cent target, however the Bank expressed concerns over the state of the economy.

Interest Rates and the Canadian Housing Market

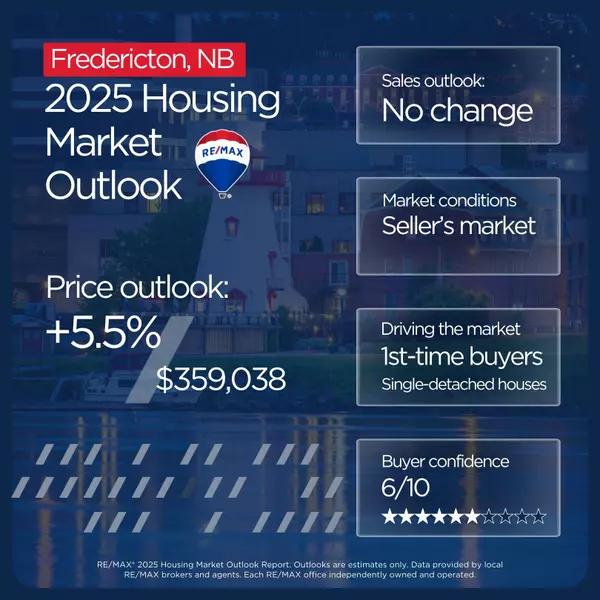

The 2025 housing market is on the rebound, according to the latest outlook from RE/MAX Canada. Canadians are looking ahead to 2025 with a more positive outlook on the housing market, initially prompted by a series of interest rate cuts in the latter part of 2024, and with further cuts expected in 2025. With buyers expected to come off the sidelines, sellers have already started listing more properties for sale. The national average residential price is expected to increase by five per cent next year, with sales anticipated to increase in 33 or 37 major markets surveyed, with increases in activity of up to 25 per cent.

While affordability challenges persist, the sequential interest rate cuts and changes to the mortgage stress test are a much-needed reprieve for those looking to get into the market. The current environment is more encouraging than it has been in the past few years, especially for first-time homebuyers. However, a boost in sales, coupled with limited inventory, almost always leads to rising prices, which is the trend we’re expecting to see materialize in virtually all Canadian housing markets.

Bank of Canada’s 2025 Policy Interest Rate Announcement Schedule

Bank of Canada announces its decision for the overnight rate target eight times a year, typically on a Wednesday. The schedule for 2025 is as follows:

- Wednesday, January 29

- Wednesday, March 12

- Wednesday, April 16

- Wednesday, June 4

- Wednesday, July 30

- Wednesday, September 17

- Wednesday, October 29

- Wednesday, December 10

Read the full interest rate announcement below:

The Bank of Canada today reduced its target for the overnight rate to 3¼%, with the Bank Rate at 3½% and the deposit rate at 3¼%. The Bank is continuing its policy of balance sheet normalization.

The global economy is evolving largely as expected in the Bank’s October Monetary Policy Report (MPR). In the United States, the economy continues to show broad-based strength, with robust consumption and a solid labour market. US inflation has been holding steady, with some price pressures persisting. In the euro area, recent indicators point to weaker growth. In China, recent policy actions combined with strong exports are supporting growth, but household spending remains subdued. Global financial conditions have eased and the Canadian dollar has depreciated in the face of broad-based strength in the US dollar.

In Canada, the economy grew by 1% in the third quarter, somewhat below the Bank’s October projection, and the fourth quarter also looks weaker than projected. Third-quarter GDP growth was pulled down by business investment, inventories and exports. In contrast, consumer spending and housing activity both picked up, suggesting lower interest rates are beginning to boost household spending. Historical revisions to the National Accounts have increased the level of GDP over the past three years, largely reflecting higher investment and consumption. The unemployment rate rose to 6.8% in November as employment continued to grow more slowly than the labour force. Wage growth showed some signs of easing, but remains elevated relative to productivity.

A number of policy measures have been announced that will affect the outlook for near-term growth and inflation in Canada. Reductions in targeted immigration levels suggest GDP growth next year will be below the Bank’s October forecast. The effects on inflation will likely be more muted, given that lower immigration dampens both demand and supply. Other federal and provincial policies—including a temporary suspension of the GST on some consumer products, one-time payments to individuals, and changes to mortgage rules—will affect the dynamics of demand and inflation. The Bank will look through effects that are temporary and focus on underlying trends to guide its policy decisions.

In addition, the possibility the incoming US administration will impose new tariffs on Canadian exports to the United States has increased uncertainty and clouded the economic outlook.

CPI inflation has been about 2% since the summer, and is expected to average close to the 2% target over the next couple of years. Since October, the upward pressure on inflation from shelter and the downward pressure from goods prices have both moderated as expected. Looking ahead, the GST holiday will temporarily lower inflation but that will be unwound once the GST break ends. Measures of core inflation will help us assess the trend in CPI inflation.

With inflation around 2%, the economy in excess supply, and recent indicators tilted towards softer growth than projected, Governing Council decided to reduce the policy rate by a further 50 basis points to support growth and keep inflation close to the middle of the 1-3% target range. Governing Council has reduced the policy rate substantially since June. Going forward, we will be evaluating the need for further reductions in the policy rate one decision at a time. Our decisions will be guided by incoming information and our assessment of the implications for the inflation outlook. The Bank is committed to maintaining price stability for Canadians by keeping inflation close to the 2% target.

Interest Rate Announcement Archives

The Bank of Canada today reduced its target for the overnight rate to 3¾%, with the Bank Rate at 4% and the deposit rate at 3¾%. The Bank is continuing its policy of balance sheet normalization.

The Bank continues to expect the global economy to expand at a rate of about 3% over the next two years. Growth in the United States is now expected to be stronger than previously forecast while the outlook for China remains subdued. Growth in the euro area has been soft but should recover modestly next year. Inflation in advanced economies has declined in recent months, and is now around central bank targets. Global financial conditions have eased since July, in part because of market expectations of lower policy interest rates. Global oil prices are about $10 lower than assumed in the July Monetary Policy Report (MPR).

In Canada, the economy grew at around 2% in the first half of the year and we expect growth of 1¾% in the second half. Consumption has continued to grow but is declining on a per person basis. Exports have been boosted by the opening of the Trans Mountain Expansion pipeline. The labour market remains soft—the unemployment rate was at 6.5% in September. Population growth has continued to expand the labour force while hiring has been modest. This has particularly affected young people and newcomers to Canada. Wage growth remains elevated relative to productivity growth. Overall, the economy continues to be in excess supply.

GDP growth is forecast to strengthen gradually over the projection horizon, supported by lower interest rates. This forecast largely reflects the net effect of a gradual pick up in consumer spending per person and slower population growth. Residential investment growth is also projected to rise as strong demand for housing lifts sales and spending on renovations. Business investment is expected to strengthen as demand picks up, and exports should remain strong, supported by robust demand from the United States.

Overall, the Bank forecasts GDP growth of 1.2% in 2024, 2.1% in 2025, and 2.3% in 2026. As the economy strengthens, excess supply is gradually absorbed.

CPI inflation has declined significantly from 2.7% in June to 1.6% in September. Inflation in shelter costs remains elevated but has begun to ease. Excess supply elsewhere in the economy has reduced inflation in the prices of many goods and services. The drop in global oil prices has led to lower gasoline prices. These factors have all combined to bring inflation down. The Bank’s preferred measures of core inflation are now below 2½%. With inflationary pressures no longer broad-based, business and consumer inflation expectations have largely normalized.

The Bank expects inflation to remain close to the target over the projection horizon, with the upward and downward pressures on inflation roughly balancing out. The upward pressure from shelter and other services gradually diminishes, and the downward pressure on inflation recedes as excess supply in the economy is absorbed.

With inflation now back around the 2% target, Governing Council decided to reduce the policy rate by 50 basis points to support economic growth and keep inflation close to the middle of the 1% to 3% range. If the economy evolves broadly in line with our latest forecast, we expect to reduce the policy rate further. However, the timing and pace of further reductions in the policy rate will be guided by incoming information and our assessment of its implications for the inflation outlook. We will take decisions one meeting at a time. The Bank is committed to maintaining price stability for Canadians by keeping inflation close to the 2% target.

The Bank of Canada today reduced its target for the overnight rate to 4¼%, with the Bank Rate at 4½% and the deposit rate at 4¼%. The Bank is continuing its policy of balance sheet normalization.

The global economy expanded by about 2½% in the second quarter, consistent with projections in the Bank’s July Monetary Policy Report (MPR). In the United States, economic growth was stronger than expected, led by consumption, but the labour market has slowed. Euro-area growth has been boosted by tourism and other services, while manufacturing has been soft. Inflation in both regions continues to moderate. In China, weak domestic demand weighed on economic growth. Global financial conditions have eased further since July, with declines in bond yields. The Canadian dollar has appreciated modestly, largely reflecting a lower US dollar. Oil prices are lower than assumed in the July MPR.

In Canada, the economy grew by 2.1% in the second quarter, led by government spending and business investment. This was slightly stronger than forecast in July, but preliminary indicators suggest that economic activity was soft through June and July. The labour market continues to slow, with little change in employment in recent months. Wage growth, however, remains elevated relative to productivity.

As expected, inflation slowed further to 2.5% in July. The Bank’s preferred measures of core inflation averaged around 2 ½% and the share of components of the consumer price index growing above 3% is roughly at its historical norm. High shelter price inflation is still the biggest contributor to total inflation but is starting to slow. Inflation also remains elevated in some other services.

With continued easing in broad inflationary pressures, Governing Council decided to reduce the policy interest rate by a further 25 basis points. Excess supply in the economy continues to put downward pressure on inflation, while price increases in shelter and some other services are holding inflation up. Governing Council is carefully assessing these opposing forces on inflation. Monetary policy decisions will be guided by incoming information and our assessment of their implications for the inflation outlook. The Bank remains resolute in its commitment to restoring price stability for Canadians.

The Bank of Canada today reduced its target for the overnight rate to 4½%, with the Bank Rate at 4¾% and the deposit rate at 4½%. The Bank is continuing its policy of balance sheet normalization.

The global economy is expected to continue expanding at an annual rate of about 3% through 2026. While inflation is still above central bank targets in most advanced economies, it is forecast to ease gradually. In the United States, the anticipated economic slowdown is materializing, with consumption growth moderating. US inflation looks to have resumed its downward path. In the euro area, growth is picking up following a weak 2023. China’s economy is growing modestly, with weak domestic demand partially offset by strong exports. Global financial conditions have eased, with lower bond yields, buoyant equity prices, and robust corporate debt issuance. The Canadian dollar has been relatively stable and oil prices are around the levels assumed in April’s Monetary Policy Report (MPR).

In Canada, economic growth likely picked up to about 1½% through the first half of this year. However, with robust population growth of about 3%, the economy’s potential output is still growing faster than GDP, which means excess supply has increased. Household spending, including both consumer purchases and housing, has been weak. There are signs of slack in the labour market. The unemployment rate has risen to 6.4%, with employment continuing to grow more slowly than the labour force and job seekers taking longer to find work. Wage growth is showing some signs of moderating, but remains elevated.

GDP growth is forecast to increase in the second half of 2024 and through 2025. This reflects stronger exports and a recovery in household spending and business investment as borrowing costs ease. Residential investment is expected to grow robustly. With new government limits on admissions of non-permanent residents, population growth should slow in 2025.

Overall, the Bank forecasts GDP growth of 1.2% in 2024, 2.1% in 2025, and 2.4% in 2026. The strengthening economy will gradually absorb excess supply through 2025 and into 2026.

CPI inflation moderated to 2.7% in June after increasing in May. Broad inflationary pressures are easing. The Bank’s preferred measures of core inflation have been below 3% for several months and the breadth of price increases across components of the CPI is now near its historical norm. Shelter price inflation remains high, driven by rent and mortgage interest costs, and is still the biggest contributor to total inflation. Inflation is also elevated in services that are closely affected by wages, such as restaurants and personal care.

The Bank’s preferred measures of core inflation are expected to slow to about 2½% in the second half of 2024 and ease gradually through 2025. The Bank expects CPI inflation to come down below core inflation in the second half of this year, largely because of base year effects on gasoline prices. As those effects wear off, CPI inflation may edge up again before settling around the 2% target next year.

With broad price pressures continuing to ease and inflation expected to move closer to 2%, Governing Council decided to reduce the policy interest rate by a further 25 basis points. Ongoing excess supply is lowering inflationary pressures. At the same time, price pressures in some important parts of the economy—notably shelter and some other services—are holding inflation up. Governing Council is carefully assessing these opposing forces on inflation. Monetary policy decisions will be guided by incoming information and our assessment of their implications for the inflation outlook. The Bank remains resolute in its commitment to restoring price stability for Canadians.

The Bank of Canada today reduced its target for the overnight rate to 4¾%, with the Bank Rate at 5% and the deposit rate at 4¾%. The Bank is continuing its policy of balance sheet normalization.

The global economy grew by about 3% in the first quarter of 2024, broadly in line with the Bank’s April Monetary Policy Report (MPR) projection. In the United States, the economy expanded more slowly than was expected, as weakness in exports and inventories weighed on activity. Growth in private domestic demand remained strong but eased. In the euro area, activity picked up in the first quarter of 2024. China’s economy was also stronger in the first quarter, buoyed by exports and industrial production, although domestic demand remained weak. Inflation in most advanced economies continues to ease, although progress towards price stability is bumpy and is proceeding at different speeds across regions. Oil prices have averaged close to the MPR assumptions, and financial conditions are little changed since April.

In Canada, economic growth resumed in the first quarter of 2024 after stalling in the second half of last year. At 1.7%, first-quarter GDP growth was slower than forecast in the MPR. Weaker inventory investment dampened activity. Consumption growth was solid at about 3%, and business investment and housing activity also increased. Labour market data show businesses continue to hire, although employment has been growing at a slower pace than the working-age population. Wage pressures remain but look to be moderating gradually. Overall, recent data suggest the economy is still operating in excess supply.

CPI inflation eased further in April, to 2.7%. The Bank’s preferred measures of core inflation also slowed and three-month measures suggest continued downward momentum. Indicators of the breadth of price increases across components of the CPI have moved down further and are near their historical average. However, shelter price inflation remains high.

With continued evidence that underlying inflation is easing, Governing Council agreed that monetary policy no longer needs to be as restrictive and reduced the policy interest rate by 25 basis points. Recent data has increased our confidence that inflation will continue to move towards the 2% target. Nonetheless, risks to the inflation outlook remain. Governing Council is closely watching the evolution of core inflation and remains particularly focused on the balance between demand and supply in the economy, inflation expectations, wage growth, and corporate pricing behaviour. The Bank remains resolute in its commitment to restoring price stability for Canadians.

The Bank of Canada today held its target for the overnight rate at 5%, with the Bank Rate at 5¼% and the deposit rate at 5%. The Bank is continuing its policy of quantitative tightening.

The Bank expects the global economy to continue growing at a rate of about 3%, with inflation in most advanced economies easing gradually. The US economy has again proven stronger than anticipated, buoyed by resilient consumption and robust business and government spending. US GDP growth is expected to slow in the second half of this year, but remain stronger than forecast in January. The euro area is projected to gradually recover from current weak growth. Global oil prices have moved up, averaging about $5 higher than assumed in the January Monetary Policy Report (MPR). Since January, bond yields have increased but, with narrower corporate credit spreads and sharply higher equity markets, overall financial conditions have eased.

The Bank has revised up its forecast for global GDP growth to 2¾% in 2024 and about 3% in 2025 and 2026. Inflation continues to slow across most advanced economies, although progress will likely be bumpy. Inflation rates are projected to reach central bank targets in 2025.

In Canada, economic growth stalled in the second half of last year and the economy moved into excess supply. A broad range of indicators suggest that labour market conditions continue to ease. Employment has been growing more slowly than the working-age population and the unemployment rate has risen gradually, reaching 6.1% in March. There are some recent signs that wage pressures are moderating.

Economic growth is forecast to pick up in 2024. This largely reflects both strong population growth and a recovery in spending by households. Residential investment is strengthening, responding to continued robust demand for housing. The contribution to growth from spending by governments has also increased. Business investment is projected to recover gradually after considerable weakness in the second half of last year. The Bank expects exports to continue to grow solidly through 2024.

Overall, the Bank forecasts GDP growth of 1.5% in 2024, 2.2% in 2025, and 1.9% in 2026. The strengthening economy will gradually absorb excess supply through 2025 and into 2026.

CPI inflation slowed to 2.8% in February, with easing in price pressures becoming more broad-based across goods and services. However, shelter price inflation is still very elevated, driven by growth in rent and mortgage interest costs. Core measures of inflation, which had been running around 3½%, slowed to just over 3% in February, and 3-month annualized rates are suggesting downward momentum. The Bank expects CPI inflation to be close to 3% during the first half of this year, move below 2½% in the second half, and reach the 2% inflation target in 2025.

Based on the outlook, Governing Council decided to hold the policy rate at 5% and to continue to normalize the Bank’s balance sheet. While inflation is still too high and risks remain, CPI and core inflation have eased further in recent months. The Council will be looking for evidence that this downward momentum is sustained. Governing Council is particularly watching the evolution of core inflation, and continues to focus on the balance between demand and supply in the economy, inflation expectations, wage growth, and corporate pricing behaviour. The Bank remains resolute in its commitment to restoring price stability for Canadians.

The Bank of Canada today held its target for the overnight rate at 5%, with the Bank Rate at 5¼% and the deposit rate at 5%. The Bank is continuing its policy of quantitative tightening.

Global economic growth slowed in the fourth quarter. US GDP growth also slowed but remained surprisingly robust and broad-based, with solid contributions from consumption and exports. Euro area economic growth was flat at the end of the year after contracting in the third quarter. Inflation in the United States and the euro area continued to ease. Bond yields have increased since January while corporate credit spreads have narrowed. Equity markets have risen sharply. Global oil prices are slightly higher than what was assumed in the January Monetary Policy Report (MPR).

In Canada, the economy grew in the fourth quarter by more than expected, although the pace remained weak and below potential. Real GDP expanded by 1% after contracting 0.5% in the third quarter. Consumption was up a modest 1%, and final domestic demand contracted with a large decline in business investment. A strong increase in exports boosted growth. Employment continues to grow more slowly than the population, and there are now some signs that wage pressures may be easing. Overall, the data point to an economy in modest excess supply.

CPI inflation eased to 2.9% in January, as goods price inflation moderated further. Shelter price inflation remains elevated and is the biggest contributor to inflation. Underlying inflationary pressures persist: year-over-year and three-month measures of core inflation are in the 3% to 3.5% range, and the share of CPI components growing above 3% declined but is still above the historical average. The Bank continues to expect inflation to remain close to 3% during the first half of this year before gradually easing.

Governing Council decided to hold the policy rate at 5% and to continue to normalize the Bank’s balance sheet. The Council is still concerned about risks to the outlook for inflation, particularly the persistence in underlying inflation. Governing Council wants to see further and sustained easing in core inflation and continues to focus on the balance between demand and supply in the economy, inflation expectations, wage growth, and corporate pricing behaviour. The Bank remains resolute in its commitment to restoring price stability for Canadians.

The Bank of Canada today held its target for the overnight rate at 5%, with the Bank Rate at 5¼% and the deposit rate at 5%. The Bank is continuing its policy of quantitative tightening.

The global economy continues to slow and inflation has eased further. In the United States, growth has been stronger than expected, led by robust consumer spending, but is likely to weaken in the months ahead as past policy rate increases work their way through the economy. Growth in the euro area has weakened and, combined with lower energy prices, this has reduced inflationary pressures. Oil prices are about $10-per-barrel lower than was assumed in the October Monetary Policy Report (MPR). Financial conditions have also eased, with long-term interest rates unwinding some of the sharp increases seen earlier in the autumn. The US dollar has weakened against most currencies, including Canada’s.

In Canada, economic growth stalled through the middle quarters of 2023. Real GDP contracted at a rate of 1.1% in the third quarter, following growth of 1.4% in the second quarter. Higher interest rates are clearly restraining spending: consumption growth in the last two quarters was close to zero, and business investment has been volatile but essentially flat over the past year. Exports and inventory adjustment subtracted from GDP growth in the third quarter, while government spending and new home construction provided a boost. The labour market continues to ease: job creation has been slower than labour force growth, job vacancies have declined further, and the unemployment rate has risen modestly. Even so, wages are still rising by 4-5%. Overall, these data and indicators for the fourth quarter suggest the economy is no longer in excess demand.

The slowdown in the economy is reducing inflationary pressures in a broadening range of goods and services prices. Combined with the drop in gasoline prices, this contributed to the easing of CPI inflation to 3.1% in October. However, shelter price inflation has picked up, reflecting faster growth in rent and other housing costs along with the continued contribution from elevated mortgage interest costs. In recent months, the Bank’s preferred measures of core inflation have been around 3½-4%, with the October data coming in towards the lower end of this range.

With further signs that monetary policy is moderating spending and relieving price pressures, Governing Council decided to hold the policy rate at 5% and to continue to normalize the Bank’s balance sheet. Governing Council is still concerned about risks to the outlook for inflation and remains prepared to raise the policy rate further if needed. Governing Council wants to see further and sustained easing in core inflation, and continues to focus on the balance between demand and supply in the economy, inflation expectations, wage growth, and corporate pricing behaviour. The Bank remains resolute in its commitment to restoring price stability for Canadians.

The Bank of Canada today held its target for the overnight rate at 5%, with the Bank Rate at 5¼% and the deposit rate at 5%. The Bank is continuing its policy of quantitative tightening.

The global economy is slowing and growth is forecast to moderate further as past increases in policy rates and the recent surge in global bond yields weigh on demand. The Bank projects global GDP growth of 2.9% this year, 2.3% in 2024 and 2.6% in 2025. While this global growth outlook is little changed from the July Monetary Policy Report (MPR), the composition has shifted, with the US economy proving stronger and economic activity in China weaker than expected. Growth in the euro area has slowed further. Inflation has been easing in most economies, as supply bottlenecks resolve and weaker demand relieves price pressures. However, with underlying inflation persisting, central banks continue to be vigilant. Oil prices are higher than was assumed in July, and the war in Israel and Gaza is a new source of geopolitical uncertainty.

In Canada, there is growing evidence that past interest rate increases are dampening economic activity and relieving price pressures. Consumption has been subdued, with softer demand for housing, durable goods and many services. Weaker demand and higher borrowing costs are weighing on business investment. The surge in Canada’s population is easing labour market pressures in some sectors while adding to housing demand and consumption. In the labour market, recent job gains have been below labour force growth and job vacancies have continued to ease. However, the labour market remains on the tight side and wage pressures persist. Overall, a range of indicators suggest that supply and demand in the economy are now approaching balance.

After averaging 1% over the past year, economic growth is expected to continue to be weak for the next year before increasing in late 2024 and through 2025. The near-term weakness in growth reflects both the broadening impact of past increases in interest rates and slower foreign demand. The subsequent pickup is driven by household spending as well as stronger exports and business investment in response to improving foreign demand. Spending by governments contributes materially to growth over the forecast horizon. Overall, the Bank expects the Canadian economy to grow by 1.2% this year, 0.9% in 2024 and 2.5% in 2025.

CPI inflation has been volatile in recent months—2.8% in June, 4.0% in August, and 3.8% in September. Higher interest rates are moderating inflation in many goods that people buy on credit, and this is spreading to services. Food inflation is easing from very high rates. However, in addition to elevated mortgage interest costs, inflation in rent and other housing costs remains high. Near-term inflation expectations and corporate pricing behaviour are normalizing only gradually, and wages are still growing around 4% to 5%. The Bank’s preferred measures of core inflation show little downward momentum.

In the Bank’s October projection, CPI inflation is expected to average about 3½% through the middle of next year before gradually easing to 2% in 2025. Inflation returns to target about the same time as in the July projection, but the near-term path is higher because of energy prices and ongoing persistence in core inflation.

With clearer signs that monetary policy is moderating spending and relieving price pressures, Governing Council decided to hold the policy rate at 5% and to continue to normalize the Bank’s balance sheet. However, Governing Council is concerned that progress towards price stability is slow and inflationary risks have increased, and is prepared to raise the policy rate further if needed. Governing Council wants to see downward momentum in core inflation, and continues to be focused on the balance between demand and supply in the economy, inflation expectations, wage growth and corporate pricing behaviour. The Bank remains resolute in its commitment to restoring price stability for Canadians.

The Bank of Canada announced today it is holding its target for the overnight rate at 5%, with the Bank Rate at 5¼% and the deposit rate at 5%. The Bank is also continuing its policy of quantitative tightening.

Inflation in advanced economies has continued to come down, but with measures of core inflation still elevated, major central banks remain focused on restoring price stability. Global growth slowed in the second quarter of 2023, largely reflecting a significant deceleration in China. With ongoing weakness in the property sector undermining confidence, growth prospects in China have diminished. In the United States, growth was stronger than expected, led by robust consumer spending. In Europe, strength in the service sector supported growth, offsetting an ongoing contraction in manufacturing. Global bond yields have risen, reflecting higher real interest rates, and international oil prices are higher than was assumed in the July Monetary Policy Report (MPR).

The Canadian economy has entered a period of weaker growth, which is needed to relieve price pressures. Economic growth slowed sharply in the second quarter of 2023, with output contracting by 0.2% at an annualized rate. This reflected a marked weakening in consumption growth and a decline in housing activity, as well as the impact of wildfires in many regions of the country. Household credit growth slowed as the impact of higher rates restrained spending among a wider range of borrowers. Final domestic demand grew by 1% in the second quarter, supported by government spending and a boost to business investment. The tightness in the labour market has continued to ease gradually. However, wage growth has remained around 4% to 5%.

Recent CPI data indicate that inflationary pressures remain broad-based. After easing to 2.8% in June, CPI inflation moved up to 3.3% in July, averaging close to 3% in line with the Bank’s projection. With the recent increase in gasoline prices, CPI inflation is expected to be higher in the near term before easing again. Year-over-year and three-month measures of core inflation are now both running at about 3.5%, indicating there has been little recent downward momentum in underlying inflation. The longer high inflation persists, the greater the risk that elevated inflation becomes entrenched, making it more difficult to restore price stability.

With recent evidence that excess demand in the economy is easing, and given the lagged effects of monetary policy, Governing Council decided to hold the policy interest rate at 5% and continue to normalize the Bank’s balance sheet. However, Governing Council remains concerned about the persistence of underlying inflationary pressures, and is prepared to increase the policy interest rate further if needed. Governing Council will continue to assess the dynamics of core inflation and the outlook for CPI inflation. In particular, we will be evaluating whether the evolution of excess demand, inflation expectations, wage growth and corporate pricing behavior are consistent with achieving the 2% inflation target. The Bank remains resolute in its commitment to restoring price stability for Canadians.

The Bank of Canada announced today it is increasing its target for the overnight rate to 5%, with the Bank Rate at 5¼% and the deposit rate at 5%. The Bank is also continuing its policy of quantitative tightening.

Global inflation is easing, with lower energy prices and a decline in goods price inflation. However, robust demand and tight labour markets are causing persistent inflationary pressures in services. Economic growth has been stronger than expected, especially in the United States, where consumer and business spending has been surprisingly resilient. After a surge in early 2023, China’s economic growth is softening, with slowing exports and ongoing weakness in its property sector. Growth in the euro area is effectively stalled: while the service sector continues to grow, manufacturing is contracting. Global financial conditions have tightened, with bond yields up in North America and Europe as major central banks signal further interest rate increases may be needed to combat inflation.

The Bank’s July Monetary Policy Report (MPR) projects the global economy will grow by around 2.8% this year and 2.4% in 2024, followed by 2.7% growth in 2025.

Canada’s economy has been stronger than expected, with more momentum in demand. Consumption growth has been surprisingly strong at 5.8% in the first quarter. While the Bank expects consumer spending to slow in response to the cumulative increase in interest rates, recent retail trade and other data suggest more persistent excess demand in the economy. In addition, the housing market has seen some pickup. New construction and real estate listings are lagging demand, which is adding pressure to prices. In the labour market, there are signs of more availability of workers, but conditions remain tight, and wage growth has been around 4-5%. Strong population growth from immigration is adding both demand and supply to the economy: newcomers are helping to ease the shortage of workers while also boosting consumer spending and adding to demand for housing.

As higher interest rates continue to work their way through the economy, the Bank expects economic growth to slow, averaging around 1% through the second half of this year and the first half of next year. This implies real GDP growth of 1.8% in 2023 and 1.2% in 2024. The economy will move into modest excess supply early next year before growth picks up to 2.4% in 2025.

Inflation in Canada eased to 3.4% in May, a substantial and welcome drop from its peak of 8.1% last summer. While CPI inflation has come down largely as expected so far this year, the downward momentum has come more from lower energy prices, and less from easing underlying inflation. With the large price increases of last year out of the annual data, there will be less near-term downward momentum in CPI inflation. Moreover, with three-month rates of core inflation running around 3½-4% since last September, underlying price pressures appear to be more persistent than anticipated. This is reinforced by the Bank’s business surveys, which find businesses are still increasing their prices more frequently than normal.

In the July MPR projection, CPI inflation is forecast to hover around 3% for the next year before gradually declining to 2% in the middle of 2025. This is a slower return to target than was forecast in the January and April projections. Governing Council remains concerned that progress towards the 2% target could stall, jeopardizing the return to price stability.

In light of the accumulation of evidence that excess demand and elevated core inflation are both proving more persistent, and taking into account its revised outlook for economic activity and inflation, Governing Council decided to increase the policy interest rate to 5%. Quantitative tightening is complementing the restrictive stance of monetary policy and normalizing the Bank’s balance sheet. Governing Council will continue to assess the dynamics of core inflation and the outlook for CPI inflation. In particular, we will be evaluating whether the evolution of excess demand, inflation expectations, wage growth and corporate pricing behaviour are consistent with achieving the 2% inflation target. The Bank remains resolute in its commitment to restoring price stability for Canadians.

The Bank of Canada today increased its target for the overnight rate to 4¾%, with the Bank Rate at 5% and the deposit rate at 4¾%. The Bank is also continuing its policy of quantitative tightening.

Globally, consumer price inflation is coming down, largely reflecting lower energy prices compared to a year ago, but underlying inflation remains stubbornly high. While economic growth around the world is softening in the face of higher interest rates, major central banks are signalling that interest rates may have to rise further to restore price stability. In the United States, the economy is slowing, although consumer spending remains surprisingly resilient and the labour market is still tight. Economic growth has essentially stalled in Europe but upward pressure on core prices is persisting. Growth in China is expected to slow after surging in the first quarter. Financial conditions have tightened back to those seen before the bank failures in the United States and Switzerland.

Canada’s economy was stronger than expected in the first quarter of 2023, with GDP growth of 3.1%. Consumption growth was surprisingly strong and broad-based, even after accounting for the boost from population gains. Demand for services continued to rebound. In addition, spending on interest-sensitive goods increased and, more recently, housing market activity has picked up. The labour market remains tight: higher immigration and participation rates are expanding the supply of workers but new workers have been quickly hired, reflecting continued strong demand for labour. Overall, excess demand in the economy looks to be more persistent than anticipated.

CPI inflation ticked up in April to 4.4%, the first increase in 10 months, with prices for a broad range of goods and services coming in higher than expected. Goods price inflation increased, despite lower energy costs. Services price inflation remained elevated, reflecting strong demand and a tight labour market. The Bank continues to expect CPI inflation to ease to around 3% in the summer, as lower energy prices feed through and last year’s large price gains fall out of the yearly data. However, with three-month measures of core inflation running in the 3½-4% range for several months and excess demand persisting, concerns have increased that CPI inflation could get stuck materially above the 2% target.

Based on the accumulation of evidence, Governing Council decided to increase the policy interest rate, reflecting our view that monetary policy was not sufficiently restrictive to bring supply and demand back into balance and return inflation sustainably to the 2% target. Quantitative tightening is complementing the restrictive stance of monetary policy and normalizing the Bank’s balance sheet. Governing Council will continue to assess the dynamics of core inflation and the outlook for CPI inflation. In particular, we will be evaluating whether the evolution of excess demand, inflation expectations, wage growth and corporate pricing behaviour are consistent with achieving the inflation target. The Bank remains resolute in its commitment to restoring price stability for Canadians.

The Bank of Canada has announced today that it’s holding its target for the overnight rate at 4½%, with the Bank Rate at 4¾% and the deposit rate at 4½%. The Bank is also continuing its policy of quantitative tightening.

Inflation in many countries is easing in the face of lower energy prices, normalizing global supply chains, and tighter monetary policy. At the same time, labour markets remain tight and measures of core inflation in many advanced economies suggest persistent price pressures, especially for services.

Global economic growth has been stronger than anticipated. Growth in the United States and Europe has surprised on the upside, but is expected to weaken as tighter monetary policy continues to feed through those economies. In the United States, recent stress in the banking sector has tightened credit conditions further. US growth is expected to slow considerably in the coming months, with particular weakness in sectors that are important for Canadian exports. Meanwhile, activity in China’s economy has rebounded, particularly in services. Overall, commodity prices are close to their January levels. The Bank’s April Monetary Policy Report (MPR) projects global growth of 2.6% this year, 2.1% in 2024, and 2.8% in 2025.

In Canada, demand is still exceeding supply and the labour market remains tight. Economic growth in the first quarter looks to be stronger than was projected in January, with a bounce in exports and solid consumption growth. While the Bank’s Business Outlook Survey suggests acute labour shortages are starting to ease, wage growth is still elevated relative to productivity growth. Strong population gains are adding to labour supply and supporting employment growth while also boosting aggregate consumption. Housing market activity remains subdued.

As more households renew their mortgages at higher rates and restrictive monetary policy works its way through the economy more broadly, consumption is expected to moderate this year. Softening foreign demand is expected to restrain exports and business investment. Overall, GDP growth is projected to be weak through the remainder of this year before strengthening gradually next year. This implies the economy will move into excess supply in the second half of this year. The Bank now projects Canada’s economy to grow by 1.4% this year and 1.3% in 2024 before picking up to 2.5% in 2025.

CPI inflation eased to 5.2% in February, and the Bank’s preferred measures of core inflation were just under 5%. The Bank expects CPI inflation to fall quickly to around 3% in the middle of this year and then decline more gradually to the 2% target by the end of 2024. Recent data is reinforcing Governing Council’s confidence that inflation will continue to decline in the next few months. However, getting inflation the rest of the way back to 2% could prove to be more difficult because inflation expectations are coming down slowly, service price inflation and wage growth remain elevated, and corporate pricing behaviour has yet to normalize. As it sets monetary policy, Governing Council will be particularly focused on these indicators, and the evolution of core inflation, to gauge the progress of CPI inflation back to target.

In light of its outlook for growth and inflation, Governing Council decided to maintain the policy rate at 4½%. Quantitative tightening continues to complement this restrictive stance. Governing Council continues to assess whether monetary policy is sufficiently restrictive to relieve price pressures and remains prepared to raise the policy rate further if needed to return inflation to the 2% target. The Bank remains resolute in its commitment to restoring price stability for Canadians.

The Bank of Canada today held its target for the overnight rate at 4½%, with the Bank Rate at 4¾% and the deposit rate at 4½%. The Bank is also continuing its policy of quantitative tightening.

Global economic developments have evolved broadly in line with the outlook in the January Monetary Policy Report (MPR). Global growth continues to slow, and inflation, while still too high, is coming down due primarily to lower energy prices. In the United States and Europe, near-term outlooks for growth and inflation are both somewhat higher than expected in January. In particular, labour markets remain tight, and elevated core inflation is persisting. Growth in China is rebounding in the first quarter. Commodity prices have evolved roughly in line with the Bank’s expectations, but the strength of China’s recovery and the impact of Russia’s war in Ukraine remain key sources of upside risk. Financial conditions have tightened since January, and the US dollar has strengthened.

In Canada, economic growth came in flat in the fourth quarter of 2022, lower than the Bank projected. With consumption, government spending and net exports all increasing, the weaker-than-expected GDP was largely because of a sizeable slowdown in inventory investment. Restrictive monetary policy continues to weigh on household spending, and business investment has weakened alongside slowing domestic and foreign demand.

The labour market remains very tight. Employment growth has been surprisingly strong, the unemployment rate remains near historic lows, and job vacancies are elevated. Wages continue to grow at 4% to 5%, while productivity has declined in recent quarters.

Inflation eased to 5.9% in January, reflecting lower price increases for energy, durable goods and some services. Price increases for food and shelter remain high, causing continued hardship for Canadians. With weak economic growth for the next couple of quarters, pressures in product and labour markets are expected to ease. This should moderate wage growth and also increase competitive pressures, making it more difficult for businesses to pass on higher costs to consumers.

Overall, the latest data remains in line with the Bank’s expectation that CPI inflation will come down to around 3% in the middle of this year. Year-over-year measures of core inflation ticked down to about 5%, and 3-month measures are around 3½%. Both will need to come down further, as will short-term inflation expectations, to return inflation to the 2% target.

At its January decision, the Governing Council indicated that it expected to hold the policy interest rate at its current level, conditional on economic developments evolving broadly in line with the MPR outlook. Based on its assessment of recent data, Governing Council decided to maintain the policy rate at 4½%. Quantitative tightening is complementing this restrictive stance. Governing Council will continue to assess economic developments and the impact of past interest rate increases, and is prepared to increase the policy rate further if needed to return inflation to the 2% target. The Bank remains resolute in its commitment to restoring price stability for Canadians.

The Bank of Canada has announced today that it is increasing its target for the overnight rate to 4½%, with the Bank Rate at 4¾% and the deposit rate at 4½%. The Bank is also continuing its policy of quantitative tightening.

Global inflation remains high and broad-based. Inflation is coming down in many countries, largely reflecting lower energy prices as well as improvements in global supply chains. In the United States and Europe, economies are slowing but proving more resilient than was expected at the time of the Bank’s October Monetary Policy Report (MPR). China’s abrupt lifting of COVID-19 restrictions has prompted an upward revision to the growth forecast for China and poses an upside risk to commodity prices. Russia’s war on Ukraine remains a significant source of uncertainty. Financial conditions remain restrictive but have eased since October, and the Canadian dollar has been relatively stable against the US dollar.

The Bank estimates the global economy grew by about 3½% in 2022, and will slow to about 2% in 2023 and 2½% in 2024. This projection is slightly higher than October’s.

In Canada, recent economic growth has been stronger than expected and the economy remains in excess demand. Labour markets are still tight: the unemployment rate is near historic lows and businesses are reporting ongoing difficulty finding workers. However, there is growing evidence that restrictive monetary policy is slowing activity, especially household spending. Consumption growth has moderated from the first half of 2022 and housing market activity has declined substantially. As the effects of interest rate increases continue to work through the economy, spending on consumer services and business investment are expected to slow. Meanwhile, weaker foreign demand will likely weigh on exports. This overall slowdown in activity will allow supply to catch up with demand.

The Bank estimates Canada’s economy grew by 3.6% in 2022, slightly stronger than was projected in October. Growth is expected to stall through the middle of 2023, picking up later in the year. The Bank expects GDP growth of about 1% in 2023 and about 2% in 2024, little changed from the October outlook.

Inflation has declined from 8.1% in June to 6.3% in December, reflecting lower gasoline prices and, more recently, moderating prices for durable goods. Despite this progress, Canadians are still feeling the hardship of high inflation in their essential household expenses, with persistent price increases for food and shelter. Short-term inflation expectations remain elevated. Year-over-year measures of core inflation are still around 5%, but 3-month measures of core inflation have come down, suggesting that core inflation has peaked.

Inflation is projected to come down significantly this year. Lower energy prices, improvements in global supply conditions, and the effects of higher interest rates on demand are expected to bring CPI inflation down to around 3% in the middle of this year and back to the 2% target in 2024.

With persistent excess demand putting continued upward pressure on many prices, Governing Council decided to increase the policy interest rate by a further 25 basis points. The Bank’s ongoing program of quantitative tightening is complementing the restrictive stance of the policy rate. If economic developments evolve broadly in line with the MPR outlook, Governing Council expects to hold the policy rate at its current level while it assesses the impact of the cumulative interest rate increases. Governing Council is prepared to increase the policy rate further if needed to return inflation to the 2% target, and remains resolute in its commitment to restoring price stability for Canadians.

The Bank of Canada announced today that it is increasing its target for the overnight rate to 3.75%. Read the full announcement below:

The Bank of Canada today increased its target for the overnight rate to 3¾%, with the Bank Rate at 4% and the deposit rate at 3¾%. The Bank is also continuing its policy of quantitative tightening.

Inflation around the world remains high and broadly based. This reflects the strength of the global recovery from the pandemic, a series of global supply disruptions, and elevated commodity prices, particularly for energy, which have been pushed up by Russia’s attack on Ukraine. The strength of the US dollar is adding to inflationary pressures in many countries. Tighter monetary policies aimed at controlling inflation are weighing on economic activity around the world. As economies slow and supply disruptions ease, global inflation is expected to come down.

In the United States, labour markets remain very tight even as restrictive financial conditions are slowing economic activity. The Bank projects no growth in the US economy through most of next year. In the euro area, the economy is forecast to contract in the quarters ahead, largely due to acute energy shortages. China’s economy appears to have picked up after the recent round of pandemic lockdowns, although ongoing challenges related to its property market will continue to weigh on growth. Overall, the Bank projects that global growth will slow from 3% in 2022 to about 1½% in 2023, and then pick back up to roughly 2½% in 2024. This is a slower pace of growth than was projected in the Bank’s July Monetary Policy Report (MPR).

In Canada, the economy continues to operate in excess demand and labour markets remain tight. The demand for goods and services is still running ahead of the economy’s ability to supply them, putting upward pressure on domestic inflation. Businesses continue to report widespread labour shortages and, with the full reopening of the economy, strong demand has led to a sharp rise in the price of services.

The effects of recent policy rate increases by the Bank are becoming evident in interest-sensitive areas of the economy: housing activity has retreated sharply, and spending by households and businesses is softening. Also, the slowdown in international demand is beginning to weigh on exports. Economic growth is expected to stall through the end of this year and the first half of next year as the effects of higher interest rates spread through the economy. The Bank projects GDP growth will slow from 3¼% this year to just under 1% next year and 2% in 2024.

In the last three months, CPI inflation has declined from 8.1% to 6.9%, primarily due to a fall in gasoline prices. However, price pressures remain broadly based, with two-thirds of CPI components increasing more than 5% over the past year. The Bank’s preferred measures of core inflation are not yet showing meaningful evidence that underlying price pressures are easing. Near-term inflation expectations remain high, increasing the risk that elevated inflation becomes entrenched.

The Bank expects CPI inflation to ease as higher interest rates help rebalance demand and supply, price pressures from global supply disruptions fade, and the past effects of higher commodity prices dissipate. CPI inflation is projected to move down to about 3% by the end of 2023, and then return to the 2% target by the end of 2024.

Given elevated inflation and inflation expectations, as well as ongoing demand pressures in the economy, the Governing Council expects that the policy interest rate will need to rise further. Future rate increases will be influenced by our assessments of how tighter monetary policy is working to slow demand, how supply challenges are resolving, and how inflation and inflation expectations are responding. Quantitative tightening is complementing increases in the policy rate. We are resolute in our commitment to restore price stability for Canadians and will continue to take action as required to achieve the 2% inflation target.

The Bank of Canada announced today that it is increasing its target for the overnight rate to 3¼%, with the Bank Rate at 3½% and the deposit rate at 3¼%. The Bank is also continuing its policy of quantitative tightening.

The global and Canadian economies are evolving broadly in line with the Bank’s July projection. The effects of COVID-19 outbreaks, ongoing supply disruptions, and the war in Ukraine continue to dampen growth and boost prices.

Global inflation remains high and measures of core inflation are moving up in most countries. In response, central banks around the world continue to tighten monetary policy. Economic activity in the United States has moderated, although the US labour market remains tight. China is facing ongoing challenges from COVID shutdowns. Commodity prices have been volatile: oil, wheat and lumber prices have moderated while natural gas prices have risen.

In Canada, CPI inflation eased in July to 7.6% from 8.1% because of a drop in gasoline prices. However, inflation excluding gasoline increased and data indicate a further broadening of price pressures, particularly in services. The Bank’s core measures of inflation continued to move up, ranging from 5% to 5.5% in July. Surveys suggest that short-term inflation expectations remain high. The longer this continues, the greater the risk that elevated inflation becomes entrenched.

The Canadian economy continues to operate in excess demand and labour markets remain tight. Canada’s GDP grew by 3.3% in the second quarter. While this was somewhat weaker than the Bank had projected, indicators of domestic demand were very strong – consumption grew by about 9½% and business investment was up by close to 12%. With higher mortgage rates, the housing market is pulling back as anticipated, following unsustainable growth during the pandemic. The Bank continues to expect the economy to moderate in the second half of this year, as global demand weakens and tighter monetary policy here in Canada begins to bring demand more in line with supply.

Given the outlook for inflation, the Governing Council still judges that the policy interest rate will need to rise further. Quantitative tightening is complementing increases in the policy rate. As the effects of tighter monetary policy work through the economy, we will be assessing how much higher interest rates need to go to return inflation to target. The Governing Council remains resolute in its commitment to price stability and will continue to take action as required to achieve the 2% inflation target.

The Bank of Canada announced it is increasing its target for the overnight rate to 2½%, with the Bank Rate at 2¾% and the deposit rate at 2½%. The Bank is also continuing its policy of quantitative tightening (QT).

Inflation in Canada is higher and more persistent than the Bank expected in its April Monetary Policy Report (MPR), and will likely remain around 8% in the next few months. While global factors such as the war in Ukraine and ongoing supply disruptions have been the biggest drivers, domestic price pressures from excess demand are becoming more prominent. More than half of the components that make up the CPI are now rising by more than 5%. With this broadening of price pressures, the Bank’s core measures of inflation have moved up to between 3.9% and 5.4%. Also, surveys indicate more consumers and businesses are expecting inflation to be higher for longer, raising the risk that elevated inflation becomes entrenched in price- and wage-setting. If that occurs, the economic cost of restoring price stability will be higher.

Global inflation is higher, reflecting the impact of the Russian invasion of Ukraine, ongoing supply constraints, and strong demand. Many central banks are tightening monetary policy to combat inflation, and the resulting tighter financial conditions are moderating economic growth. In the United States, high inflation and rising interest rates are contributing to a slowdown in domestic demand. China’s economy is being held back by waves of restrictive measures to contain COVID-19 outbreaks. Oil prices remain high and volatile. The Bank now expects global economic growth to slow to about 3½% this year and 2% in 2023 before strengthening to 3% in 2024.

Further excess demand has built up in the Canadian economy. Labour markets are tight with a record low unemployment rate, widespread labour shortages, and increasing wage pressures. With strong demand, businesses are passing on higher input and labour costs by raising prices. Consumption is robust, led by a rebound in spending on hard-to-distance services. Business investment is solid and exports are being boosted by elevated commodity prices. The Bank estimates that GDP grew by about 4% in the second quarter. Growth is expected to slow to about 2% in the third quarter as consumption growth moderates and housing market activity pulls back following unsustainable strength during the pandemic.

The Bank expects Canada’s economy to grow by 3½% in 2022, 1¾% in 2023, and 2½% in 2024. Economic activity will slow as global growth moderates and tighter monetary policy works its way through the economy. This, combined with the resolution of supply disruptions, will bring demand and supply back into balance and alleviate inflationary pressures. Global energy prices are also projected to decline. The July outlook has inflation starting to come back down later this year, easing to about 3% by the end of next year and returning to the 2% target by the end of 2024.

With the economy clearly in excess demand, inflation high and broadening, and more businesses and consumers expecting high inflation to persist for longer, the Governing Council decided to front-load the path to higher interest rates by raising the policy rate by 100 basis points today. The Governing Council continues to judge that interest rates will need to rise further, and the pace of increases will be guided by the Bank’s ongoing assessment of the economy and inflation. Quantitative tightening continues and is complementing increases in the policy interest rate. The Governing Council is resolute in its commitment to price stability and will continue to take action as required to achieve the 2% inflation target.

The Bank of Canada today increased its target for the overnight rate to 1½%, with the Bank Rate at 1¾% and the deposit rate at 1½%. The Bank is also continuing its policy of quantitative tightening (QT).

Inflation globally and in Canada continues to rise, largely driven by higher prices for energy and food. In Canada, CPI inflation reached 6.8% for the month of April – well above the Bank’s forecast – and will likely move even higher in the near term before beginning to ease. As pervasive input price pressures feed through into consumer prices, inflation continues to broaden, with core measures of inflation ranging between 3.2% and 5.1%. Almost 70% of CPI categories now show inflation above 3%. The risk of elevated inflation becoming entrenched has risen. The Bank will use its monetary policy tools to return inflation to target and keep inflation expectations well anchored.

The increase in global inflation is occurring as the global economy slows. The Russian invasion of Ukraine, China’s COVID-related lockdowns, and ongoing supply disruptions are all weighing on activity and boosting inflation. The war has increased uncertainty and is putting further upward pressure on prices for energy and agricultural commodities. This is dampening the outlook, particularly in Europe. In the United States, private domestic demand remains robust, despite the economy contracting in the first quarter of 2022. US labour market strength continues, with wage pressures intensifying. Global financial conditions have tightened and markets have been volatile.

Canadian economic activity is strong and the economy is clearly operating in excess demand. National accounts data for the first quarter of 2022 showed GDP growth of 3.1 percent, in line with the Bank’s April Monetary Policy Report (MPR) projection. Job vacancies are elevated, companies are reporting widespread labour shortages, and wage growth has been picking up and broadening across sectors. Housing market activity is moderating from exceptionally high levels. With consumer spending in Canada remaining robust and exports anticipated to strengthen, growth in the second quarter is expected to be solid.

With the economy in excess demand, and inflation persisting well above target and expected to move higher in the near term, the Governing Council continues to judge that interest rates will need to rise further. The policy interest rate remains the Bank’s primary monetary policy instrument, with quantitative tightening acting as a complementary tool. The pace of further increases in the policy rate will be guided by the Bank’s ongoing assessment of the economy and inflation, and the Governing Council is prepared to act more forcefully if needed to meet its commitment to achieve the 2% inflation target.

The Bank of Canada has announced that it is increasing its target for the overnight rate to 1%, with the Bank Rate at 1¼% and the deposit rate at 1%. The Bank is also ending reinvestment and will begin quantitative tightening (QT), effective April 25. Maturing Government of Canada bonds on the Bank’s balance sheet will no longer be replaced and, as a result, the size of the balance sheet will decline over time.

Russia’s ongoing invasion of Ukraine is causing unimaginable human suffering and new economic uncertainty. Price spikes in oil, natural gas and other commodities are adding to inflation around the world. Supply disruptions resulting from the war are also exacerbating ongoing supply constraints and weighing on activity. These factors are the primary drivers of a substantial upward revision to the Bank’s outlook for inflation in Canada.

The war in Ukraine is disrupting the global recovery, just as most economies are emerging from the impact of the Omicron variant of COVID-19. European countries are more directly impacted by confidence effects and supply dislocations caused by the war. China’s economy is facing new COVID outbreaks and an ongoing correction in its property market. In the United States, domestic demand remains very strong and the US Federal Reserve has clearly indicated its resolve to use its monetary policy tools to control inflation. As policy stimulus is withdrawn, US growth is expected to moderate to a pace more in line with potential growth. Global financial conditions have tightened and volatility has increased. The Bank now forecasts global growth of about 3½% this year, 2½% in 2023 and 3¼% in 2024.

In Canada, growth is strong and the economy is moving into excess demand. Labour markets are tight, and wage growth is back to its pre-pandemic pace and rising. Businesses increasingly report they are having difficulty meeting demand, and are able to pass on higher input costs by increasing prices. While the COVID-19 virus continues to mutate and circulate, high rates of vaccination have reduced its health and economic impacts. Growth looks to have been stronger in the first quarter than projected in January and is likely to pick up in the second quarter. Consumer spending is strengthening with the lifting of pandemic containment measures. Exports and business investment will continue to recover, supported by strong foreign demand and high commodity prices. Housing market activity, which has been exceptionally high, is expected to moderate.

The Bank forecasts that Canada’s economy will grow by 4¼% this year before slowing to 3¼% in 2023 and 2¼% in 2024. Robust business investment, labour productivity growth and higher immigration will add to the economy’s productive capacity, while higher interest rates should moderate growth in domestic demand.

CPI inflation in Canada is 5.7%, above the Bank’s forecast in its January Monetary Policy Report (MPR). Inflation is being driven by rising energy and food prices and supply disruptions, in combination with strong global and domestic demand. Core measures of inflation have all moved higher as price pressures broaden. CPI inflation is now expected to average almost 6% in the first half of 2022 and remain well above the control range throughout this year. It is then expected to ease to about 2½% in the second half of 2023 and return to the 2% target in 2024. There is an increasing risk that expectations of elevated inflation could become entrenched. The Bank will use its monetary policy tools to return inflation to target and keep inflation expectations well-anchored.

With the economy moving into excess demand and inflation persisting well above target, the Governing Council judges that interest rates will need to rise further. The policy interest rate is the Bank’s primary monetary policy instrument, and quantitative tightening will complement increases in the policy rate. The timing and pace of further increases in the policy rate will be guided by the Bank’s ongoing assessment of the economy and its commitment to achieving the 2% inflation target.

From the Bank of Canada: The Bank of Canada today increased its target for the overnight rate to ½ %, with the Bank Rate at ¾ % and the deposit rate at ½ %. The Bank is continuing its reinvestment phase, keeping its overall holdings of Government of Canada bonds on its balance sheet roughly constant until such time as it becomes appropriate to allow the size of its balance sheet to decline.

The unprovoked invasion of Ukraine by Russia is a major new source of uncertainty. Prices for oil and other commodities have risen sharply. This will add to inflation around the world, and negative impacts on confidence and new supply disruptions could weigh on global growth. Financial market volatility has increased. The situation remains fluid and we are following events closely.

Global economic data has come in broadly in line with projections in the Bank’s January Monetary Policy Report (MPR). Economies are emerging from the impact of the Omicron variant of COVID-19 more quickly than expected, although the virus continues to circulate and the possibility of new variants remains a concern. Demand is robust, particularly in the United States. Global supply bottlenecks remain challenging, although there are indications that some constraints have eased.

Economic growth in Canada was very strong in the fourth quarter of last year at 6.7%. This is stronger than the Bank’s projection and confirms its view that economic slack has been absorbed. Both exports and imports have picked up, consistent with solid global demand. In January, the recovery in Canada’s labour market suffered a setback due to the Omicron variant, with temporary layoffs in service sectors and elevated employee absenteeism. However, the rebound from Omicron now appears to be well in train: household spending is proving resilient and should strengthen further with the lifting of public health restrictions. Housing market activity is more elevated, adding further pressure to house prices. Overall, first-quarter growth is now looking more solid than previously projected.

CPI inflation is currently at 5.1%, as expected in January, and remains well above the Bank’s target range. Price increases have become more pervasive, and measures of core inflation have all risen. Poor harvests and higher transportation costs have pushed up food prices. The invasion of Ukraine is putting further upward pressure on prices for both energy and food-related commodities. All told, inflation is now expected to be higher in the near term than projected in January. Persistently elevated inflation is increasing the risk that longer-run inflation expectations could drift upwards. The Bank will use its monetary policy tools to return inflation to the 2% target and keep inflation expectations well-anchored.

The policy rate is the Bank’s primary monetary policy instrument. As the economy continues to expand and inflation pressures remain elevated, the Governing Council expects interest rates will need to rise further. The Governing Council will also be considering when to end the reinvestment phase and allow its holdings of Government of Canada bonds to begin to shrink. The resulting quantitative tightening (QT) would complement increases in the policy interest rate. The timing and pace of further increases in the policy rate, and the start of QT, will be guided by the Bank’s ongoing assessment of the economy and its commitment to achieving the 2% inflation target.

Canadian real estate prices expected to continue rising

Rumours of an imminent interest rate hike did not materialize, as the Bank of Canada opted to maintain its benchmark rate at a record-low 0.25 per cent in its scheduled interest rate announcement today. The move (or lack thereof) comes despite soaring inflation and a stronger-than-expected economic recovery. The Bank noted that economic slack has been absorbed, but said the Omicron variant of COVID-19 continues to weigh on growth.

Globally, good are in high demand, with supply-chain disruptions impeding production and transportation pushing inflation upward. The Bank projected global GDP growth to ease from 6¾ per cent in last year, to 3½ per cent in 2022 and 2023.

Meanwhile, Canada’s economy proved stronger than expected in the third and fourth quarters, rounding out 2021 at +4½ per cent. Entering 2022, the Bank highlighted economic momentum, pointing to employment growth, a tighter labour market, job vacancies, strong hiring intentions and rising wages as positive factors. The Bank forecasts Canada’s economy to grow by four per cent this year and another 3½ per cent in 2023.

“CPI inflation remains well above the target range and core measures of inflation have edged up since October. Persistent supply constraints are feeding through to a broader range of goods prices and, combined with higher food and energy prices, are expected to keep CPI inflation close to five per cent in the first half of 2022. As supply shortages diminish, inflation is expected to decline reasonably quickly to about three per cent by the end of this year and then gradually ease towards the target over the projection period,” said the Bank. “Near-term inflation expectations have moved up, but longer-run expectations remain anchored on the two-per-cent target.”

On a final note, the Bank also expects elevated housing market activity to continue putting upward pressure on prices, which aligns with the 2022 Housing Market Outlook, where RE/MAX Canada anticipated average residential prices in the Canadian real estate market to increase 9.2 per cent this year, amidst high demand and a severe housing supply shortage.

The next Bank of Canada interest rate announcement is scheduled for March 2, 2022.

The Bank of Canada today held its target for the overnight rate at the effective lower bound of ¼ percent, with the Bank Rate at ½ percent and the deposit rate at ¼ percent. The Bank’s extraordinary forward guidance on the path for the overnight rate is being maintained. The Bank is continuing its reinvestment phase, keeping its overall holdings of Government of Canada bonds roughly constant.

The global economy continues to recover from the effects of the COVID-19 pandemic. Economic growth in the United States has accelerated, led by consumption, while growth in some other regions is moderating after a strong third quarter. Inflation has increased further in many countries, reflecting strong demand for goods amid ongoing supply disruptions. The new Omicron COVID-19 variant has prompted a tightening of travel restrictions in many countries and a decline in oil prices, and has injected renewed uncertainty. Accommodative financial conditions are still supporting economic activity.

Canada’s economy grew by about 5½ percent in the third quarter, as expected. Together with a downward revision to the second quarter, this brings the level of GDP to about 1½ percent below its level in the last quarter of 2019, before the pandemic began. Third-quarter growth was led by a rebound in consumption, particularly services, as restrictions were further eased and higher vaccination rates improved confidence. Persistent supply bottlenecks continued to inhibit growth in other components of GDP, including non-commodity exports and business investment.

Recent economic indicators suggest the economy had considerable momentum into the fourth quarter. This includes broad-based job gains in recent months that have brought the employment rate essentially back to its pre-pandemic level. Job vacancies remain elevated and wage growth has also picked up. Housing activity had been moderating, but appears to be regaining strength, notably in resales. The devastating floods in British Columbia and uncertainties arising from the Omicron variant could weigh on growth by compounding supply chain disruptions and reducing demand for some services.

CPI inflation is elevated and the impact of global supply constraints is feeding through to a broader range of goods prices. The effects of these constraints on prices will likely take some time to work their way through, given existing supply backlogs. Gasoline prices, which had been a major factor pushing up CPI inflation, have recently declined. Meanwhile, core measures of inflation are little changed since September. The Bank continues to expect CPI inflation to remain elevated in the first half of 2022 and ease back towards 2 percent in the second half of the year. The Bank is closely watching inflation expectations and labour costs to ensure that the forces pushing up prices do not become embedded in ongoing inflation.

The Governing Council judges that in view of ongoing excess capacity, the economy continues to require considerable monetary policy support. We remain committed to holding the policy interest rate at the effective lower bound until economic slack is absorbed so that the 2 percent inflation target is sustainably achieved. In the Bank’s October projection, this happens sometime in the middle quarters of 2022. We will provide the appropriate degree of monetary policy stimulus to support the recovery and achieve the inflation target.